Cash counters in use: advantages and key functions

1. Why are money counting machines used, and in what areas?

Money counters are used in all the places where companies wish to count, check, sort and pack large quantities of cash. Automating these processes rather than performing them manually makes them more secure, efficient and cost-effective: Counterfeits are identified more reliably, manual counting and checking processes are no longer required, administrative effort is reduced, and strain is taken off employees. All of this strengthens customer confidence in cash processing. Banks, cash-in-transit companies, and casinos use cash counters in almost all functional areas, from the counter to their back office or cash center; when cash is put into or removed from circulation; as well as on all transport routes. Cash counting machines are mainly used for back office operations elsewhere in industry – for example in the retail trade, catering, at gas stations or by transport operators. These devices reduce employee workload arising from routine tasks such as counting daily takings, sorting notes and coins, bundling, and identifying counterfeit money.

2. What advantages do cash counting machines offer over manual counting?

Money counters can count large quantities of cash very much more quickly than employees can by hand. They also don’t ever lose count. This makes cash processes – such as payments in and out of the counter, loading ATMs, or daily closing of tills – significantly more secure and efficient, as well as being more cost-effective for the company. It saves time and resources. Cash counters perform several tasks at once: as well as counting, they also simultaneously check whether coins and notes are authentic. They sort banknotes by criteria such as currency denomination, and can recognize that a banknote is damaged and needs to be withdrawn. Advanced cash counting machines can also read serial numbers while counting.

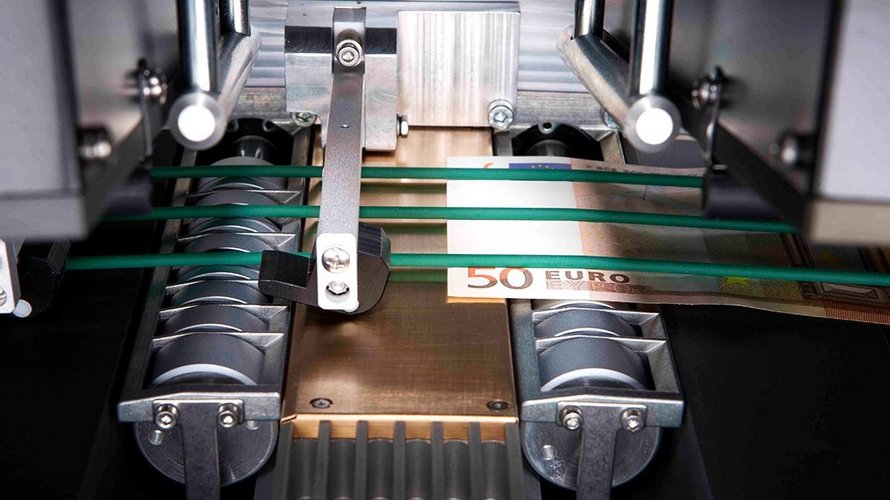

3. How do money counters work?

In banknote counting machines, banknotes are placed into the insertion compartment. Using negative pressure, the notes are then individually suctioned out of the feeder and directed through the device via mechanical transport equipment such as endless conveyor belts, idler pulleys, and diverter pulleys, as well as pivoting gates. Banknote counting machines have highly sensitive sensors that enable them to check the optical, physical, and chemical features of each individual banknote. This relates to properties such as numbers and characters, colors, length, and width, but also security features such as security thread, and infrared or magnetic properties. The notes are then sorted into a range of output trays. The data determined appear on the display. Coin counting machines work in line with a similar principle. Coins are checked for authenticity, counted, and sorted based on their thickness and diameter, as well as the metal alloy used. As is the case with all cash counters, coin counters also have high-grade sensors.

4. How do money counters for different target groups differ?

a) For banks

All types of money counters are used in central and commercial banks: compact devices on counters in branches and in the back office, and high-performance systems in large cash centers. Machines for use in central and large cash centers are certified separately, for example in the European Central Bank (ECB) area. At counters and in the back office, money counting machines should support the respective processes performed by branch employees when providing customer support. They are easy to use and feature dust-repellent and noise-reducing housing, as well as interfaces with additional IT systems. Cash counters in a bank can verify banknotes using several security features. As a result, they reliably detect even well-made counterfeits. In addition, they sort soiled and damaged banknotes which are no longer fit for circulation.

b) For casinos

Casinos use money counters in two areas: in count rooms where the daily proceeds from gambling tables and gaming machines are counted and verified, and at the cash registers where visitors buy and redeem playing chips. Requirements differ greatly between these areas. Count rooms need to work quickly, precisely and reliably. The quantities of cash they process are very large, and often consist of different currencies, with notes and coins of varying condition. For these reasons, large, powerful systems are used – like the BPS M5 from G+D – that can verify, count, sort, and band up to 2,000 banknotes per minute across a huge range of currencies. The machines support various operation modes and cash processes. On the other hand, easy-to-use table-top devices are essential at casino cash registers, as there is the space available in cash register boxes is scarce. In addition to functions such as authentication, accounting, and sorting, cash counters also perform tasks such as cashing up, counting foreign currencies, and sort control.

c) For Small and Medium Enterprises (SME)

SMEs use all types of money counters, depending on their business area. The spectrum ranges from mini-format cash testing equipment with which taxi drivers check the authenticity of their passengers’ notes; through compact floor-mounted devices which cash-in-transit companies use to verify banknotes; to high-performance systems with which professional cash centers process their customers’ cash sales and cash in circulation. Depending on the customer, cash counters are aligned to the areas of use and specific requirements of SMEs.

d) For the retail trade

Money counters that are used in the retail trade are one thing above all else: compact. Space-saving design is at least as important as ease-of-use. Requirements differ when it comes to the functionality of money counting machines: some buyers just need to check banknotes or coins for authenticity, and others want to count their daily income on an automated basis. The size and range of functions offered by the devices are generally based on the quantity of cash processed. An electrical connection to central enterprise resource planning is essential for branch businesses. For the target group, it’s important that the accessories are appropriate – from external printers to displays and coin hoppers, to replacement batteries.

5. What can money counting machines do, and how quick are they?

Money counters can count and sort large quantities of cash, as well as reliably checking them for authenticity. At the same time, they check whether notes and coins are still “fit for circulation”. Heavily soiled or damaged banknotes and counterfeit coins or banknotes are automatically withdrawn. Depending on the size of the machine, it may also offer additional functions: some can process checks, others process up to ten currencies at the same time, and some can even read serial numbers or process casino tickets. The specific differences between high-performance systems and compact systems relate to speed, the degree of automation, and operational capacity. Cash counters are significantly quicker than employees counting by hand. Even compact devices, such as the ProNote® 130 from G+D, handle up to 1,500 banknotes per minute. The BPS® X9 holds the world record for cash counting – with a throughput of up to 44 banknotes per second.

6. Can cash counting machines identify counterfeit cash?

The identification of counterfeit cash is one of the most important tasks performed by money counters. After all, many counterfeits are now so well made that they can no longer be recognized with the naked eye. For this reason, banknotes and coins contain “machine-readable” security features which are reliably checked by sensors in cash counters.

7. What sets money counting machines from G+D apart?

Cash counters from G+D are among the premium systems available on the market. The sensor technologies they use offer an extremely high level of precision, and the same is true for all their hardware and software components. This makes cash counting machines from G+D particularly powerful, efficient, and secure. Machines from G+D are long-lasting, easy to use, and can grow with the requirements of their users – resulting in an excellent cost/benefit ratio.

Get in touch

If you have any questions about our end-to-end business solutions or about our SecurityTech company, seek expert advice, or want to give us your feedback, our team is here to support you, anytime.