“Cash is king,” the first-time traveler may have been told by someone who visited India a decade ago. “You’ll need cash for taxis, tips, all that street food you’ll want to eat. Shopping requires it, especially when there’s bargaining involved. Cards should work in the cities, but are hit-or-miss outside – don’t take electricity and connectivity for granted.”

This advice wouldn’t have been wrong 10 years ago. But things have changed since then in this enormous country. A quick glance around after landing at an international airport in India will confirm what even the most cursory pre-travel research will have suggested: the payment landscape has changed dramatically in the last 7–8 years.

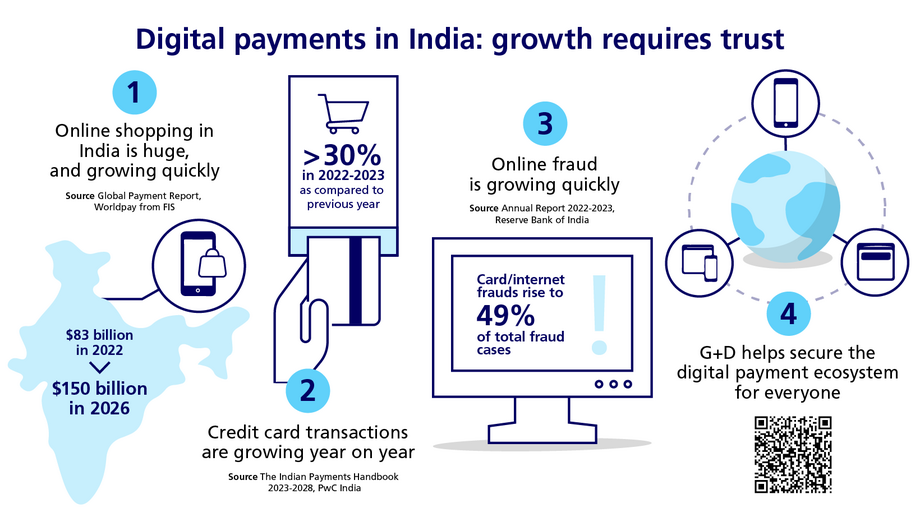

Advertisements for India’s homegrown e-commerce sites line the walk to immigration. Download the apps via QR code, enroll a payment card, and scan through the deals. Register for a local ride-hailing service while waiting for luggage. Stop at a counter helping foreign nationals register for the digital payment ecosystem that powers the new economy. Tap to pay for that last coffee before leaving the terminal. If taking a taxi, scan a QR code and pay the amount from a smartphone when the ride ends. If the passenger is getting picked up, they’ll notice the driver doesn’t have to queue up to pay for parking, or even insert a ticket in a machine – a tag on the windshield is read electronically and the money owed is automatically deducted, the process being repeated as they cross other toll plazas on the way to their final destination.

While cash is still important in the payments sphere in India – cash in circulation increased by almost 8% in 2022–2023, as compared with the previous year1 – it is clear that the digital payments sphere is evolving rapidly. Let us examine why this is so.