CBDC: Digital cash for everyone, anywhere, anytime

Everyone should have access to convenient and secure digital payments. It should be a given that they are inclusive and resilient. Central bank digital currencies (CBDCs) provide a public way to pay and store money digitally. We are here to build your national CBDC solution – one that supports all players in the payment industry.

As digital forms of payment continue to grow in number and popularity, we believe that there is a need for a government-backed digital currency that is secure and trusted. A retail CBDC is a digital version of physical cash. Issued by a central bank, it is pegged to a local currency and made available to everyone, everywhere. It has the same characteristics as cash – while providing the convenience of digital payment methods. That means it can be used for payments in stores and online, and can be easily sent to friends and family.

But beyond that – and equally important – CBDC fosters digital financial inclusion and serves as a platform for innovation by the private sector boosting the digital economy.

We concluded that there is no existing technological solution that meets the fundamental core requirements of a CBDC. This is why G+D developed its own unique and innovative retail CBDC solution G+D Filia®.

G+D is in a unique position to provide holistic CBDC solutions. As a trusted partner of central banks and financial institutions worldwide, G+D combines a deep understanding of public currencies with know-how in smart card, digital and wearable payment technologies. In addition, we offer expertise in secure connectivity and building digital infrastructures with defense-grade security. G+D is actively developing CBDC solutions together with central banks across all continents, and supporting them in building a robust and secure digital currency ecosystem.

Fundamental core requirements of a CBDC

Anonymous yet transparent

In order to be widely accepted by users and to prevent illegal payment activity, CBDC must balance anonymity with transparency. Mechanisms that prevent untaxed economies and financial crime in the physical world – none of which reduce the value of cash or restrict citizens’ freedom to make transactions – must be transferred into the digital world. And, unlike current digital payments, CBDC would not involve disclosing personal data to third parties.

Inclusive, universally accepted, and accessible

As legal tender, CBDC must be accepted by all merchants and enterprises within a country. At the same time, individuals must be able to access it without needing expensive or complicated devices. Payments must always be possible – even offline or without power supply. These are the key factors required to build trust and acceptance of CBDC among the general public.

Maximum security

Certain critical infrastructures, such as public payment, are of such vital importance to societal structure and the national economy that their failure would result in significant disruption to public security. Protecting CBDC from cyberattacks and other threats is just as important as upholding banknote security.

Our offering to make CBDC a reality

Developing a CBDC solution is a complex undertaking, and securely implementing it even more so. Our holistic understanding of financial systems combined with expertise in building highly secure digital infrastructures and digital payment know-how provides a sound basis for creating a secure CBDC solution.

Download reports

Unlocking the potential of a CBDC ecosystem

This report provides insights into the value a CBDC ecosystem can create such as efficient, programmable payments, greater security and faster cross-border remittances. Learn more about the ecosystem player, business opportunities and challenges and how can they be addressed.

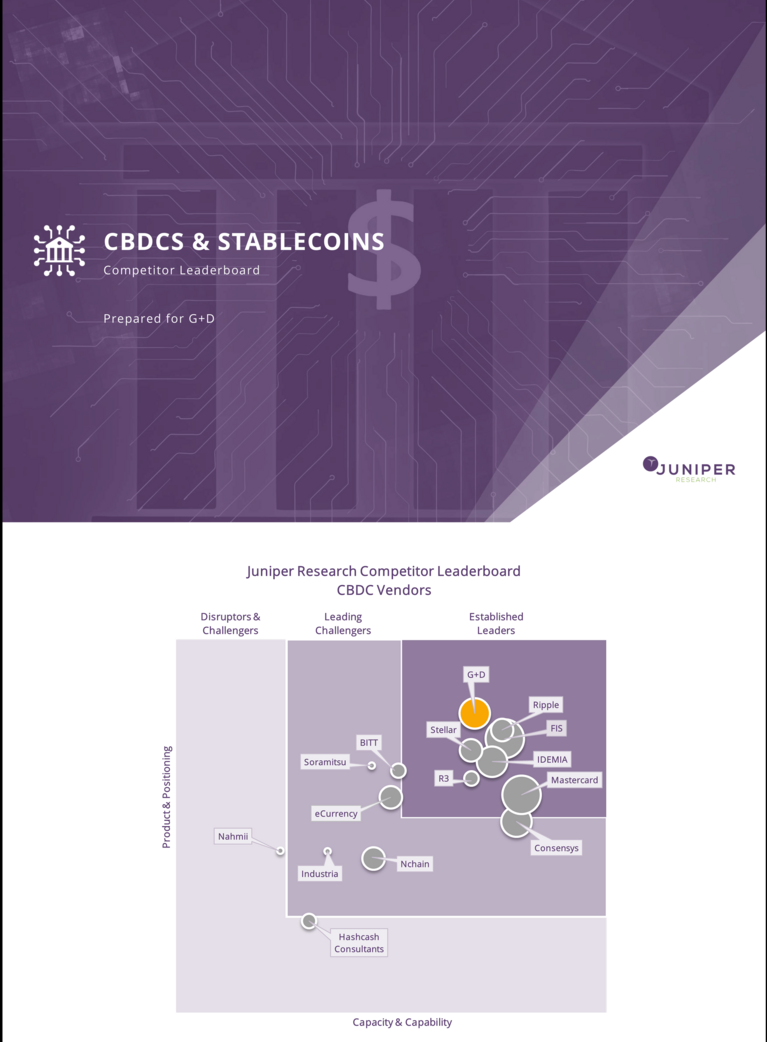

“Established Leader” in CBDC Competitor Leaderboard

G+D scored very highly on Juniper Research’s Competitor Leaderboard for CBDC Vendors. G+D was especially noted for “Creativity and Innovation” and “Future Business Prospects”. In particular, Juniper noted G+D’s legacy of being a trusted partner of numerous central banks, and its development of Filia® as a distinct product, as reasons to believe in its future success.

Financial inclusion across borders with retail CBDC

Number and value of non-commercial remittances across borders is growing as more and more migrant workers send money to friends and family back home. Cross-border payments suffer from a long list of inefficiencies and come with high fees. Cross-border retail CBDCs could positively impact this situation, making the process for sending money home quicker, cheaper, and more secure.

Consumer attitudes to CBDC

The report includes a survey conducted by Ipsos MORI on behalf of OMFIF and G+D which provides an invaluable insight into consumers’ attitudes towards a legal digital means of payment. It was conducted in four countries – Germany, Indonesia, Nigeria, and the US – with over 3,000 respondents. Findings help offer a map for policy-makers as they consider design of retail central bank digital currencies.

Proof points of our expertise

G+D wins Global CBDC Challenge

The Monetary Authority of Singapore (MAS) has declared Giesecke+Devrient (G+D) as one of the three winners of the Global Central Bank Digital Currency Challenge (Global CBDC Challenge). The judges awarded G+D’s solution Filia® for being a means of payment that can be universally used and is truly inclusive, enabling participation in the digital economy even without a smartphone or a bank account. The announcement took place at the Singapore FinTech Festival.

More insights into CBDC

Join the team

Sign up for our newsletter!

Request more information

If you have any questions about our end-to-end business solutions or about our SecurityTech company, seek expert advice, or want to give us your feedback, our team is here to support you, anytime.