Dividing up the cash cycle cake

An increasing number of central banks are transferring elements of their work to cash-in-transit companies, commercial banks and other commercial players with the objective of making cash management more efficient. But can this happen without losing control over the process?

What added value do we offer? What are our core tasks? And how can we complete them as effectively and cost-efficiently as possible? When it comes to optimizing the cash cycle, the private sector has been asking itself the same questions as the public sector and central banks for some time. Various considerations are causing them to rethink their role in the cash cycle:

Four important cash facts

- The costs of cash are increasing as the volume of cash in circulation is growing internationally by approximately 5% each year. Meanwhile, reproduction technologies are becoming more easily accessible, making it necessary to invest in security and authentication.

- Infrastructure and labor costs for cash management are rising in some countries.

- With the rise in cashless and mobile payment options, cash in public perception faces competitive pressure – also in terms of cost. Resources required to ensure a stable cash supply are ultimately borne by the general public

- Accountability in the public sector makes clear the impetus for internal and external action to ensure cash cycle effciciency

Technical and strategic adjustment levers

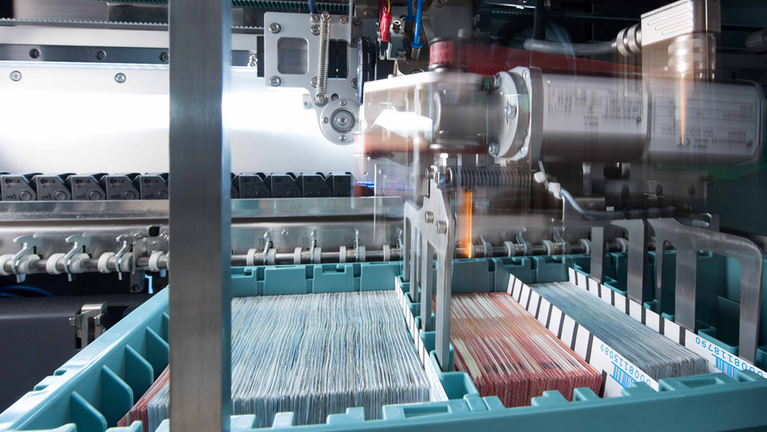

There are various levers that central banks can adjust to increase efficiency in the cash cycle and reduce costs. Some of the adjustments are technical: In banknote processing for example, smart automation solutions can be used to enhance productivity by means of higher throughput and fewer manual work steps. The use of predictive maintenance and remote services reduces downtime to a minimum. And data intelligence makes it possible to optimize sorting settings in fitness testing for example, as well as to create shredder forecasts that enable better capacity planning.

Other areas for improvement arise from questions of process and strategy: Can work steps be removed from the cash cycle? Can downstream tasks be transferred in order to enable certain areas to concentrate on more important responsibilities? And if they can, is this in line with the company’s values and objectives? Different central banks are answering these questions in different ways: Each has its own philosophy and follows its own style. On the one hand, a central bank may opt for a “controlled” style, which involves them deliberately fulfilling their key role in the cash cycle, and taking the strain off commercial banks and cash-in-transit companies by incesting in their own large-volume processing systems. At the other end of the spectrum is the “minimalistic” style, wherein the central bank transfers its day-to-day tasks to commercial players in the cash cycle. There are many additional models in between, incorporating various degrees of process outsourcing and cooperation from the public and private sector, across the entire span.

A question of cost versus risk

The key basis for decision-making when choosing one cash management model over another is individually weighing up the risks and saving potentials they facilitate. Institutions that favor the controlled style implement the technological levers described above to reduce costs. They rely on regularly updating their infrastructure, as well as using smart automated solutions and innovative data analysis applications, among other tools. They continue to perform their traditional tasks and functions, and as a result all corresponding risks remain internal and therefore in clear view. Most minimalist organizations continue the work of issuing banknotes and coins, bringing them into circulation for the first time, and destroying them when they are no longer fit for circulation – however, they are increasingly withdrawing from day-to-day fitness sorting and authentication. Why should this work be done twice, considering that it is generally performed by retailers, commercial banks, and cash-in-transit companies? Isn’t it sufficient for cash that is no longer fit for circulation to simply be returned to the central bank? Even the recirculation of deposits, and deposit facilities themselves can be taken over directly by cash-in-transit companies for example – without taking a detour to the central bank safes. Those are the arguments of central banks who operate in the minimalistic style: So they transfer the tasks mentioned to the private sector, with the goal of making cash management more efficient. However, it is critical that central banks still ensure that security and quality standards are retained and risks do not increase. Ultimately, they remain responsible for a functioning cash cycle.

How much regulation is needed?

How do central banks retain control over the processes that they no longer implement themselves? “This challenge makes it essential to have strict but fair rules and stipulations for commercial stakeholders” explains Barnabás Ferenczi, Head of Sales and Service Europe at G+D Currency Technology. “Many central banks consult with us on processing and implementation of appropriate security frameworks covering all areas from authentication and fitness verification to returning cash to circulation. In this context, it is necessary to find the right degree of regulation in each area, ensuring that neither too much nor too little is demanded from partners in the private sector.”

The European Cash Management Companies Association, ESTA, makes the case for a similar campaign in a position paper, which calls for balance sheet relief mechanisms for the storage of central bank deposits in separate safes. The paper points out that it will only be possible to perform central bank tasks cost-efficiently if the burden of interest payments is eliminated. In a separate position paper, the European Payment Council also highlights the need for balance sheet mechanisms which apply for all commercial players if they come together to perform central bank tasks in “special purpose entities”.

Which is the best cash cycle model?

Sometimes, central banks also take part in joint ventures, an intermediate model of cash cycle management. However, ESTA does not support this model, finding that it results in every partner bearing high investment costs, which ultimately do not pay off.

Transparency created through data strengthens the cornerstone of a functioning cash cycle: mutual trust among stakeholders.

Barnabás Ferenczi, Head of Sales and Service Europe at G+D Currency Technology

In contrast, Barnabás Ferenczi is firmly convinced that all models can work, and that the key to success is digitalization and data analysis. ATMs are now inter-connected, banknote processing systems collect a huge quantity of information, and now that we are in the Internet of Things age, we are very close to a platform that is able to connect all machines, systems, and players in the cash cycle. We can also use “big data” to offer crucial indications as to how the entire cash cycle can be optimized. “In addition, transparency created through data strengthens the cornerstone of a functioning cash cycle: mutual trust among stakeholders” explains Ferenczi.

No matter how the cash cycle “cake” is divided, trust is essential for maximum efficiency of the cash cycle!

Get in touch

If you have any questions about our end-to-end business solutions or about our SecurityTech company, seek expert advice, or want to give us your feedback, our team is here to support you, anytime.